Research : Loan Prediction Software for Financial Institutions

Financial institutions are focused on expanding their revenue streams, by selling various financial solutions, to their customers, a big chunk of this revenue comes from the credit line of business. The profitability of a financial institution is dependent on how well the credit business is yielding revenue, hence there is a huge focus on optimizing this process and an ardent desire to reduce the risk of loan defaulters. Adoption of AI/ML technologies are transforming credit process by significantly reducing the risk by predicting loan defaults. Data Science has paved the way for enabling predictive analytics. Several data science techniques such as Logistic regression, SVM, Neural Networks, Random Forest are discussed in this paper on how they enable increasing the accuracy of predicting loan defaulters. This paper deals with how a credit score is predicted to help financial institutions set the terms of loan disbursements to their customers. The focus of this paper is to present a loan prediction solution - Seven Seas to financial institutions. Several aspects of loan origination have been dealt with in this paper. A high-level process of loan application and an alternative credit scoring model using Machine Learning has been described. This paper also entails the overall market scope for such a solution and identifies several financial institutions that can embark on their transformation initiatives with such a disruptive technology. The extent of the existing market and its scope to embrace this technology is phenomenal not just in India but also globally.

I. INTRODUCTION

Fintech industry is on a transformation drive, the disruptions with technology adoptions have been very significant. It is no longer limited to online banking, mobile banking, telebanking etc. New age technologies based on AIML have been the crux of this digital transformation. Financial institutions are driven to provide seamless, cost effective and time sensitive solutions to stay ahead of competition. There is a constant urge to innovate, automate and transform. In the last few years we have seen almost all the banking organizations have adopted AI driven solutions such as Chat Bots, Digital Assistants, Voice technology etc. With a growing lending market- According to Allied Market Research - The global micro lending market size was valued at $134.35 billion in 2019, and is projected to reach $343.84 billion by 2027, growing at a CAGR of 12.6% from 2020 to 2027. [9]

Emerging countries have a significant growth opportunity with an increase in the number of microfinance organizations that can help reduce poverty and improve the standard of living. This market includes banks, Micro Finance Institute (MFI), NBFC (Non-Banking Financial Institutions), and others. These can be small enterprises, solo enterprises and the potential is global all across North America, Europe, Asia-Pacific, and LAMEA. In addition to the Microfinance market, Digital Lending Market is expected to register a CAGR of approximately 11.9% during the forecast period (2021 - 2026) [3]. Due to the Covid-19 pandemic, SMEs across the globe faced challenges to raise funds during the crisis to keep their businesses operating [18]. Key market trends indicate that about 2/3rd of lending is now shifting towards online platforms, with more and more players emerging in this segment due to increased digital access to consumers (borrowers) through mobiles, tablets etc.[27]. This has created tremendous potential for consumers without an existing credit history, facing challenges with loan approvals with traditional mechanisms [26], to consider digital lending platforms to a larger extent, which are much quicker and faster. [8]

Governments have also recognized the upward trend in the digital loan market and have started coming with new regulations. Few examples:

- China has seen significant growth, and over there the Government have started coming up with stringent measures [3]. China is a leading market for lending institutions and consumers (borrowers), but is also facing lot of challenges on loan repayments [29]

- India has seen a huge spike in digital lending start-ups [3]

- Japan is now offering subsidies for several online transactions to encourage use of digital platforms. [3]

II. METHODOLOGY FOR THE AI MODEL

But, the sheer nature of business being very risky, fintech firms are looking at identifying transformational technologies to reduce the overall risk in lending business. Especially with the pandemic around, financial institutions are prioritizing the credit process checks and are extensively adopting AIML based solutions to reduce the overall loan default risk. In the rest of the paper, we first provide an overview of how a lending process works in the financial industry and how AI/ML technologies can enable a low risk loan provisioning by predicting the loan defaults. It entails details [17] on how dataset is acquired for building a model, exploratory data analysis, data cleansing, data visualization, use of AI/ML techniques such as Logistic Regression, Neural Networks [24] etc. to build the model and use of performance measures such as Accuracy, ROC-AUC, Recall, Precision and F1 Score. This paper provides an overview on product development roadmap, target segment which can leverage the model to transform their business operations, SWOT Analysis, Challenges & Risk Mitigation, Team building, Go-to market strategy, pricing plans, revenue model, ROI and exit criteria.

Our road to build comprised of the following phases:

- Data Collection

- Data Pre Processing

- Data clean up

- Model Selection

- Model Scoring and Evaluation

A key component of building the Model was having the right data in place. For this purpose, we reached out to Kaggle [19] as one of the most trusted data source providers. This data set that we chose was further split into two sets viz; the training data and the other being the test data in the ratio of 70:30.

The next critical step that followed in our effort to build the AI Model was Pre-processing of data. This is a technique which transforms raw data into a more understandable, useful and efficient format. Our dataset comprises both the historic data of customers of the financial institution and that which is collected online and from the social media platforms. Included in our scope is an alternative credit scoring model [25][26] for which we identified an exhaustive list of variables. Some of these variables can also be determined to be directly related to loan defaults [22] Some of the key fields /variables that are used on the project are listed in the table below:

Table 1: Required Documents for Credit Scoring

| ID Proof | Educational certifications | Property documents | Employment history | Paytm transactions |

| Tax Returns | Insurance payments | Utility payments | CIBIL Score | Address verification status |

| Payslips | Rental receipts | Collaterals- gold, FD, Shares | Social media – SMS. India Mart, Just dial | Licenses - Commercial |

Data cleansing is performed predominantly to replace / eliminate missing values from the data sets. We then moved onto conducting exploratory data analysis, where we leveraged statistical concepts such as normal distribution, Probability density function to study the dependent and independent variables and also to detect outliers and anomalous events. We deployed the classification technique of Logistic regression, SVM, Random Forest and Artificial Neural Networks [15] to assess the credit risk. Score Model and Evaluate Model techniques are leveraged to study the accuracy and precision. The Model selection was determined keeping in mind the merits of the tools and techniques and our core mission of designing a Model which is unbiased and is fair upon evaluation.

Some of the key metrics [16] that we tracked are:

The Confusion metrics

- Accuracy

- Precision

- Recall

An accuracy score of 0.81 is seen as a good score on the AI Model. Those applicants with an overall high score are given the approval for loan while those with medium scores and higher on risk are charged a higher interest rate for the approved loan amount. Our Model attempted to provide such insights that the maximum percentage of the population is able to secure loans from the financial institutions.

III. SOLUTION DESCRIPTION

A. Credit Lending in the Bank with AI Model to predict the probability of a default

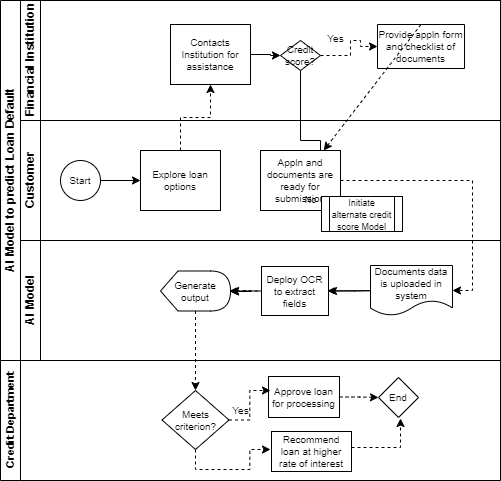

The lending process involves a series of activities that lead to the approval or rejection of a bank loan application. The First stage of Lending/Financial services is known as Loan Origination process. The most important & critical stage in complete Loan servicing. For almost every lender the definition of the term Loan origination is different – where it starts, the different stages within the process and where it ends. Every Loan type will have a different approval process that can be manual or automatic. The types of loans [2] are as listed below:

- Home loans

- Personal Loans

- Credit card loans

- Car loans

- Two wheeler loans

- Small business loans

- Payday loans

- Cash advances

7 Stages in Loan Origination

- Pre-Qualification Process: This is the first step in the Loan origination process. At this stage, the potential borrower will receive a list of items they need to submit to the lender to get a loan. This may include: ID Proof / Address proof: Voter ID, AADHAAR, PAN CARD; Current Employment Information including Salary slip; Credit Score - {subject to availability}; Bank statement & Previous Loan Statement. Once this information is submitted to the lending company, Lender reviews the documents and a pre-approval is made, allowing the borrower to continue in the process to get a loan. (** These are the fields/parameters which are inputs to the AI Model).

- Loan Application: This is the second stage of the loan origination process. In this stage, the borrower completes the loan application. Sometimes this application can be paper-based, but today lenders are shifting towards an electronic version that makes this stage Paperless. New technologies allow completing the application online through website & mobile app, and collected data can be tailored to specific loan products.

- Application Processing: At this stage, the application is received by the credit department and the first step done by the department is to review it for accuracy, genuine & Completeness. If all the required fields are not completed, the application will be returned to the borrower or the credit analyst and they will reach out to the borrower to procure the missing information. Lenders use LOAN ORIGINATION SYSTEM (LOS)[7] to know the creditworthiness of the borrowers. A good LOS will help a lender setup workflow to process a loan. It can automatically flag files with missing required fields, return it to the borrowers and notify the sales/Credit department to rework. Depending on the organization & product, exception processing might be a part of this stage.

- Underwriting Process: When an application is totally completed, the underwriting process begins. Now Lender checks the application taking a variety of components into account: credit score, risk scores, and many lenders generate their own unique criteria for scoring that can be unique to their business or industry. Nowadays, this process is fully automated with the help of a rule engine & API integrations with Credit scoring engine’s (CIBIL, EXPERIAN etc.) in LOS. In a rule engine, the lender can load underwriting guidelines specific to products.

- Credit Decision: Depending on the results from the underwriting process, an application will be approved, denied or sent back to the originator for additional information. If certain criteria don't match according to the rule engine set in the system, there can be an automatic change in the parameters, such as reduced loan amount or different interest rates.

- Quality Check: Since lending is highly regulated, the quality check stage of the loan origination process is critical to lenders. The application is sent to the quality control team that analyzes critical variables against internal and external rules and regulations. This is the last look at the application before it goes to funding.

- Loan Funding: Most loans are funded shortly after the loan documents are signed. Second mortgage loans, Business loans, Loan against property and lines of credit may require additional time for legal and compliance reasons. LOS can track funding and ensure that all necessary documents are executed before or together with funding.

B. Key Features:

- Our project aims to build an AI Model which is fair, unbiased and enables profit making. The input to the data involves an extensive list of variables/fields supported by proof of documentation.

- The Model is built using the classification technique of Logistic regression and Artificial Neural Networks. Score Model and Evaluate Model techniques are leveraged to study the accuracy and precision. [14]

1. Benefits

The deployment of the Model would result in elimination/reduction of manual intervention, reduce risk of defaults while achieving a high level of accuracy

2. USP

An inherent characteristic of any financial institution irrespective of its size is to lend money at a certain interest level which is higher than what it pays to its depositors. In parallel an individual who may belong either to a salaried class or run a business is looking to borrow money so as to meet his/her needs. Our research says there is a large segment of the population which does not hold a key parameter which is a credit score. This may be the case of a salaried individual who has got his first job [27] or/and a small-time businessman (ex: Kirana store owner) who may or may not even hold a bank account [26]. Research says the potential for this market globally is largely untapped due to lack of a structured approach to approve/reject a loan application. Our project also aims to bring under its scope this segment to help facilitate the process of lending and borrowing through a fair and unbiased approach which also results in profit sharing and thereby contributing to the economy.

As a first step we aim to design a mechanism to generate a score on similar lines of that of a credit score which will be a key component. For this purpose, we have come up with an extensive list of variables which will serve as an input to arrive at a score which the algorithm will leverage to predict probability of a loan default. [6]

C. Data & People

As our Organization embarks on its journey of AI/ML it is very critical that we have the right structure in place to help accomplish our objectives. For this purpose, we propose to have a core team of 12 members which includes the Senior Executive (1), COE (2), Data Scientist (1), Functional SME (1), Sales Lead (2), Deployment SME (1), Solution Architect, (1) Data SME (1), Model Design SME (2) and Infra support (1) We plan to scale up the team in the months to follow. Roles and responsibilities have been clearly defined for each of the resource to enable smooth execution of the Product development.

D. Product Development Roadmap and milestones

The AI/ML models we plan to leverage include Logistic Regression, Neural Networks, SVM, Random Forest to build our credit scoring model and measure the performance with ROC-AUC curve, Accuracy, Precision, Recall & F1 Score. The dataset and the variable will also influence the model we will be using for model development. Once we have a model developed this will get this deployed using the AI/Devops team and make it available as an application and as a mobile app for customers to be able to leverage the power of AI/ML.

The license to the model is being offered as SaaS, and will be available on cloud accessible through a web UI. We will ensure a legitimate & navigable friendly documentation for all the process and steps would seamlessly onboard the new users. For New customers, an FAQ document with video explanation would make the customer friendly in using our application. The training requirements for customers to use the solution will be met through detailed documentation and usage videos.

IV. EXPANSION PLAN AND EXIT STRATEGY

Once the model is in production and becomes available to the market, there is a huge scope of scaling the product both in terms of adapting newer AI enablement’s as part of the product development roadmap and as well as addressing the growing digital lending [5] and microfinance segments. The objective is to deliver a more robust, low risk, profit oriented, cost effective, seamless AI model to its customers. It has been observed that some of the existing competitive solutions are priced high and lenders are passing on the costs to the consumers, which is creating a huge dissatisfaction among them. With this lenders reputation can get compromised, which is key to sustaining a larger market share. We are looking to embark on this and provide a best in class solution with a low cost SaaS based solution. This solution opens a whole new set of opportunities to tap into customers with no credit score, many other parameters to be deployed to track customer’s financial stability, like his daily transactions, his purchase history, sales history, customer base, property ownership etc.

Every AI model keeps evolving as new data[23] gets added into the database. We have structured our pricing strategy to enable a no cost credit check component, encouraging not just the lending organization to feed the data, but also allowing the end consumers(borrowers) to register on the application to check on what their credit score looks like. This will allow for more data to be created for testing the model, thereby improving the overall model performance[28]. Over a period of time, the model will become more robust on predicting with better accuracy. As we progress, we are looking to create differentiating components for each of the loan segments – such as Home Loan, Car Loan, Two- Wheeler Loans, Personals Loans etc. No doubt our target customer is a lender for using the model, but we would aim to create an ecosystem, where the end consumer is able to receive hassle free loan processing. Key focus will be to keep improving the model and create an enabling environment both for the lender and end consumer. For example – collaborating with lenders to agree upon a minimum score criteria for loan provisioning. Adopting a model to provision a credit score certificate to end consumers – helping lender shorten their processing time and so on.

We also plan to collaborate with Fintech solutions like RuPay, PayTM, GPay, Billdesk, etc.We would like to adopt Six Sigma for continuous improvement, this will enable us to keep evolving to the market expectations and demands. With a strengthened solution and process, we aim to extend our market segment to mid-sized financial institutions, large financial institutions and global emerging markets.

B. BUSINESS PLAN (FINANCIALS)

Seven Seas - Loan Default Prediction is being offered as a SaaS to the target customers [10]. The AI model will be hosted on a cloud platform veiled behind product keys to access the AI model. The business financials have been identified as one-time set-up costs and recurring costs - which include ongoing Premises Costs, Hardware infrastructure costs, Software License costs, Marketing Costs, Human Resource costs, Contingency costs. [12]

Table 2. Initial One-time Set-up Costs

| Initial Set-up Costs | Item | Cost in USD |

|---|---|---|

| Company Registration | $750 | |

| Domain Purchase & Web hosting | $500 | |

| Contingency Costs | $250,000 | |

| Certification Costs (ISO 27001 Certification) | $11,000 | |

| Total Costs | $262,250 |

Certification Costs [20], Domain & Hosting [21]

Expenses: Seven Seas will leverage cloud hosting services to provision the hardware requirements.

Table 3. Total Annual Costs

| Annual Costs (USD) | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|

| Hardware Costs | $120,000 | $120,000 | $120,000 | $120,000 | $120,000 |

| Software Costs | $5,267 | $5,267 | $5,267 | $5,267 | $5,267 |

| HR Costs | $200,000 | $200,000 | $200,000 | $200,000 | $200,000 |

| Marketing Costs | $25,000 | $25,000 | $25,000 | $25,000 | $25,000 |

| Zoho1 Costs | $1,100 | $1,100 | $1,100 | $1,100 | $1,100 |

| Insurance Costs | $10,000 | $10,000 | $10,000 | $10,000 | $10,000 |

| Miscellaneous Costs | $25,000 | $25,000 | $25,000 | $25,000 | $25,000 |

| Total Costs | $386,367 | $386,367 | $386,367 | $386,367 | $386,367 |

| Total Cumulative Costs | $386,367 | $772,734 | $1,159,101 | $1,545,468 | $1,931,835 |

| Total Costs (Includes Initial one-time cost) | $648,617 | $772,734 | $1,159,101 | $1,545,468 | $1,931,835 |

Hardware & Software Costs [11], Insurance Costs [1], software development/HR costs [12]

Note: No separate training required for the customers. The tool usage demo/videos will be provided to enable the customers to use the solution. These costs are covered under marketing costs.

Table 4. Pricing Model [10]

| Trial Plan | Lite - Monthly Plan | Pro - Annual Plan | Premium - Enterprise Annual Plan |

|---|---|---|---|

|

• Free • One time access to report • Generate 100 Reports |

• $49.99/month • Full Access • Upto reports 1000/month • Single user |

• $149.99/month • Full Access • Upto 3000 Reports/month • 5 users • Upfront Payment |

• $599.99/month • Full Access • Upto 5,000 Reports/month • 50 users • Upfront Payment |

Table 5. Total Revenue

| Pricing | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|

| Monthly Plan (Lite) | |||||

| Targeted Revenue /Year | $ 41,991.60 | $ 89,982.00 | $ 116,976.60 | $ 152,069.58 | $ 197,690.45 |

| Annual Plan (Pro) Upfront Payment | |||||

| Targeted Revenue /Year | $ 35,998 | $ 125,992 | $ 188,987 | $ 283,481 | $ 425,222 |

| Enterprise Annual Plan (Premium) Upfront Payment | |||||

| Targeted Revenue /Year | $ 71,999 | $ 215,996 | $ 323,995 | $ 485,992 | $ 728,988 |

| Overall Targeted Revenue /Year | $ 149,988 | $ 431,970 | $ 629,959 | $ 921,543 | $ 1,351,900 |

| Overall Cumulative Revenue/Year | $ 149,988 | $ 581,958 | $ 1,211,917 | $ 2,133,459 | $ 3,485,359 |

Table 6. ROI Analysis: Estimating a Break-Even at Year 3

| ROI | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|

| Total Cumulative Expenses | $648,617 | $772,734 | $1,159,101 | $1,545,468 | $1,931,835 |

| Total Cumulative Revenue | $149,988 | $581,958 | $1,211,917 | $2,133,459 | $3,485,359 |

| ROI | ($498,629) | ($190,776) | $52,816 | $587,991 | $1,553,524 |

| ROI in % | 23% | 75% | 105% | 138% | 180% |

| Differential ROI | -77% | -25% | 5% | 38% | 80% |

C. Exit Strategy:

Seven Seas plans to start looking at exiting the business after 5 years in the business. As part of the overall strategy, we would like to get merged or acquired by a competitor (or) a business entity to take over the business. Here are the key indicators we will be looking for an exit [4]:

- Established Business Model

- Profitable Business

- Revenue – After 5 years, once cumulative revenue is doubled than that of cumulative expenses.

V. REFERENCES

- CoverWallet. (n.d.). Insurance for Startups. CoverWallet. Retrieved December 25, 2021, from https://www.coverwallet.com/general/start-ups

- Different Types of Bank Loans in India. (n.d.). Bankbazaar.Com. Retrieved December 25, 2021, from https://www.bankbazaar.com/home-loan/different-types-of-bank-loans-in-india.html

- Digital Lending Market. (n.d.). Mordorintelligence.Com. Retrieved December 25, 2021, from https://www.mordorintelligence.com/industry-reports/digital-lending-market

- Exit strategies. (2020, July 15). Corporate Finance Institute. https://corporatefinanceinstitute.com/resources/knowledge/strategy/exit-strategies-plans/

- India: digital lending value 2023. (n.d.). Statista. Retrieved December 25, 2021, from https://www.statista.com/statistics/1202533/india-digital-lending-volume/

- Kozodoi, N., Jacob, J., & Lessmann, S. (2022). Fairness in credit scoring: Assessment, implementation and profit implications. European Journal of Operational Research, 297(3), 1083–1094. https://doi.org/10.1016/j.ejor.2021.06.023

- Loan origination system. (n.d.). Allcloud.In. Retrieved December 25, 2021, from https://allcloud.in/loan-origination-system

- Mayank. (2021, June 24). A look into the digital lending market in India. LeadSquared. https://www.leadsquared.com/digital-lending-market/

- Microfinance market size, share and industry forecast - 2030. (n.d.). Allied Market Research. Retrieved December 24, 2021, from https://www.alliedmarketresearch.com/microfinance-market-A06004

- Žiaukė, K. (n.d.). Your complete guide to SaaS pricing models. Learn.G2.Com. Retrieved December 25, 2021, from https://learn.g2.com/saas-pricing-models

- Google Cloud pricing calculator. (n.d.). Google Cloud. Retrieved December 25, 2021, from https://cloud.google.com/products/calculator

- TP&P Technology. (n.d.). How much does artificial intelligence (AI) solutions development cost in 2020-2021? TP&P Technology. Retrieved December 25, 2021, from https://www.tpptechnology.com/blog/how-much-does-artificial-intelligence-ai-solutions-development-cost-in-2019/

- (N.d.). Gov.Hk. Retrieved January 14, 2022, from https://www.hkma.gov.hk/media/eng/doc/key-functions/financial-infrastructure/alternative_credit_scoring.pdf

- (N.d.-b). Mdpi.Com. Retrieved January 14, 2022, from https://www.mdpi.com/2227-9091/9/11/192/pdf

- Turiel, J. D., & Aste, T. (2020). Peer-to-peer loan acceptance and default prediction with artificial intelligence. Royal Society Open Science, 7(6), 191649. https://doi.org/10.1098/rsos.191649

- Chang, S., Simon, D.-O., & Kondo, G. (n.d.). Predicting default risk of lending Club loans. Stanford.Edu. Retrieved January 14, 2022, from http://cs229.stanford.edu/proj2015/199_report.pdf

- Sheikh, M. A., Goel, A. K., & Kumar, T. (2020). An approach for prediction of loan approval using machine learning algorithm. 2020 International Conference on Electronics and Sustainable Communication Systems (ICESC), 490–494.

- Ciampi, F., Giannozzi, A., Marzi, G., & Altman, E. I. (2021). Rethinking SME default prediction: a systematic literature review and future perspectives. Scientometrics, 126(3), 1–48. https://doi.org/10.1007/s11192-020-03856-0

- Dutta, G. (n.d.). Loan Defaulter [Data set].

- Typical ISO 27001 certification costs. (n.d.). Itgovernanceusa.Com. Retrieved January 14, 2022, from https://www.itgovernanceusa.com/iso27001-certification-costs

- VPS hosting. (n.d.). Hostgator.Com. Retrieved January 14, 2022, from https://www.hostgator.com/vps-hosting

- Zhao, S., & Zou, J. (2021). Predicting loan defaults using logistic regression. Journal of Student Research, 10(1). https://doi.org/10.47611/jsrhs.v10i1.1326

- N. Darapaneni et al., “Universal Text Scanner Solution,” in 2020 IEEE 15th International Conference on Industrial and Information Systems (ICIIS), 2020, pp. 431–436.

- Kumar, M., Goel, V., Jain, T., Singhal, S., & Goel, L. M. (n.d.). Neural network approach to loan default prediction. Irjet.Net. Retrieved February 5, 2022, from https://www.irjet.net/archives/V5/i4/IRJET-V5I4942.pdf

- Financial inclusion and alternate credit scoring for the millennials: Role of big data and machine learning in Fintech. (2020). Cam.Ac.Uk. https://www.jbs.cam.ac.uk/wp-content/uploads/2020/08/2020-06-conference-paper-agarwal-alok-ghosh-gupta.pdf

- Njuguna, R., & Sowon, K. (2021). Poster: A scoping review of alternative credit scoring literature. ACM SIGCAS Conference on Computing and Sustainable Societies (COMPASS).

- Agarwal, S., Alok, S., Ghosh, P., & Gupta, S. (2019). Fintech and credit scoring for the millennials: Evidence using mobile and social footprints. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3507827

- N. Darapaneni et al., “Handwritten form recognition using artificial neural network,” in 2020 IEEE 15th International Conference on Industrial and Information Systems (ICIIS), 2020, pp. 420–424.

- Xu, J., Lu, Z., & Xie, Y. (2021). Loan default prediction of Chinese P2P market: a machine learning methodology. Scientific Reports, 11(1), 18759. https://doi.org/10.1038/s41598-021-98361-6